Access thousands of high-converting templates, social posts, and flyers designed to help loan officers fill their pipeline and close more loans—built into Shape’s mortgage marketing CMS.

Pre-made flyers, emails, and landing pages

Social media tools with ready-to-post content

Campaigns built for every stage of the loan process

Shape’s built-in call, text, and email tools let you connect 1:1 or run bulk campaigns—all in one place, with email authentication, 10DLC compliance, and built-in spam protection.

Two-way SMS/MMS with images, videos and emojis

Built-in, compliant dialer with call tracking & scoring

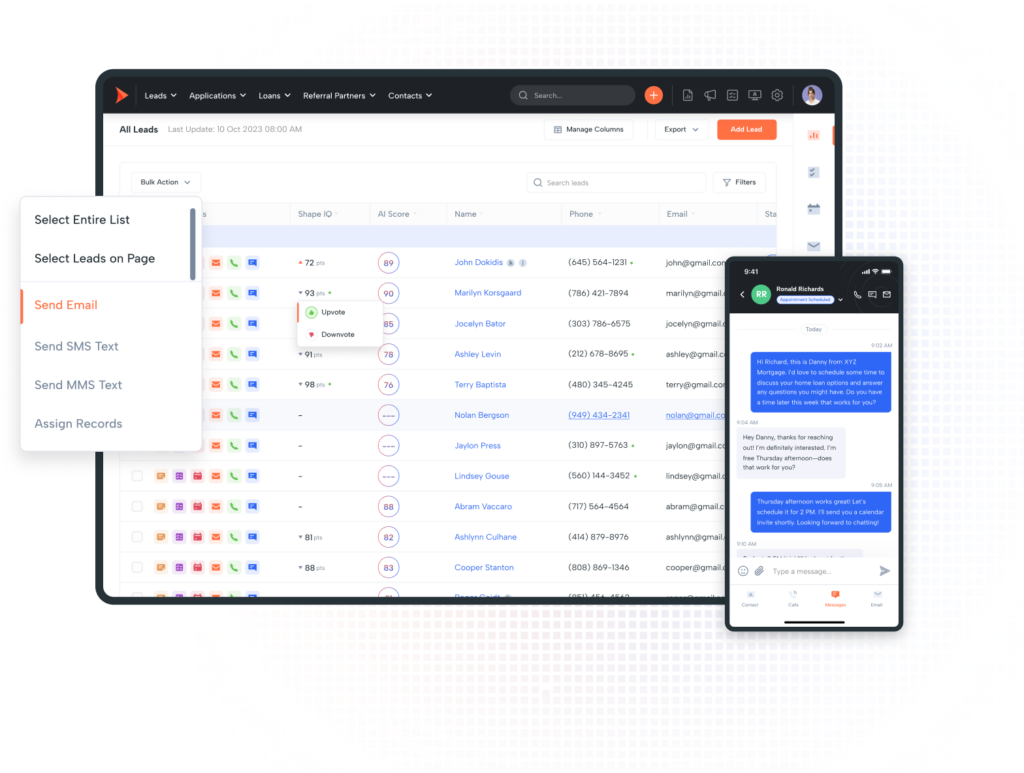

Shape’s all-in-one CRM helps mortgage teams manage leads, prioritize follow-up, and move faster with built-in communication, automation, and integrations—so nothing slips through the cracks.

Lead management with smart prioritization & routing

Built-in dialer, text, and email with full tracking

Shape’s CRO-optimized landing pages and lead funnels are fully designed, built, and maintained for you—with expert integrations that drive real results and sync directly to your mortgage CRM.

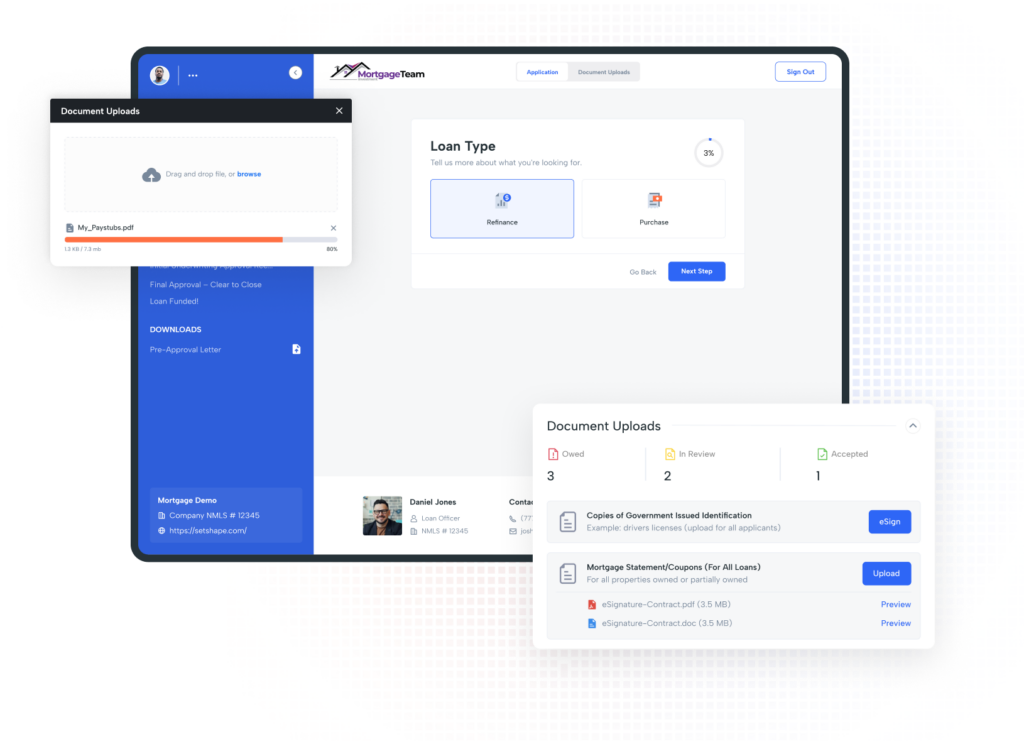

Collect borrower docs and 1003 applications in one place – synced to your LOS without extra logins, tabs, or manual work. Shape’s built-in POS helps you move faster and close with less friction.

One portal for 1003s and doc collection

Notifications and workflows that move loans forward

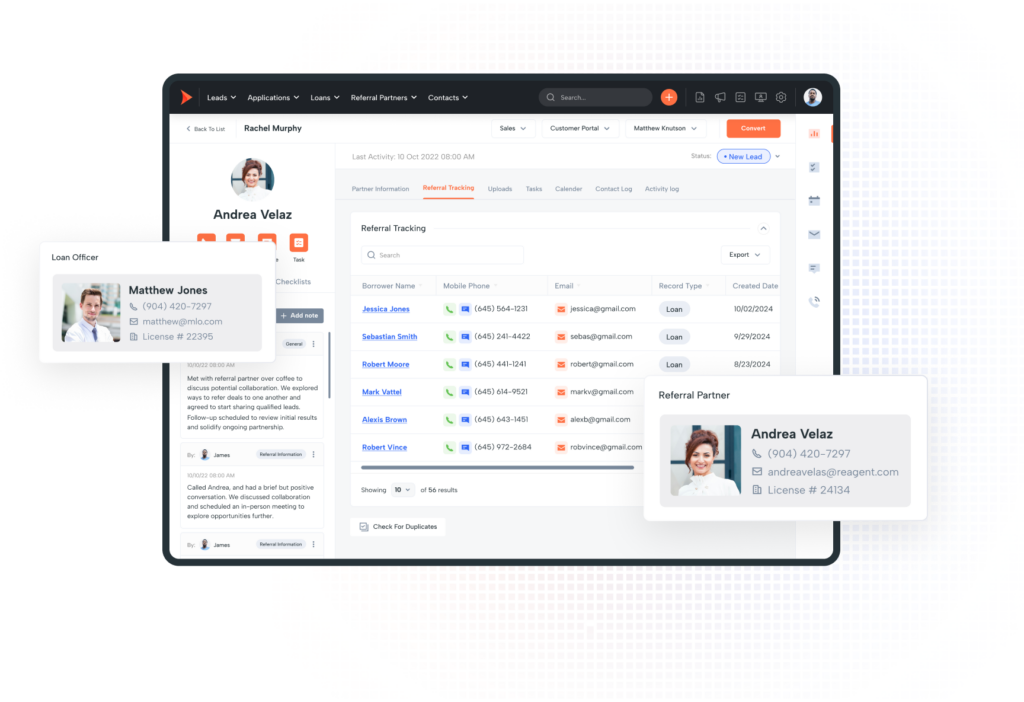

Shape’s built-in referral partner tools help you manage, prioritize, and nurture your most valuable realtor relationships—with full tracking, automation, and co-branded marketing built right in.

Identify and track top-performing referral partners

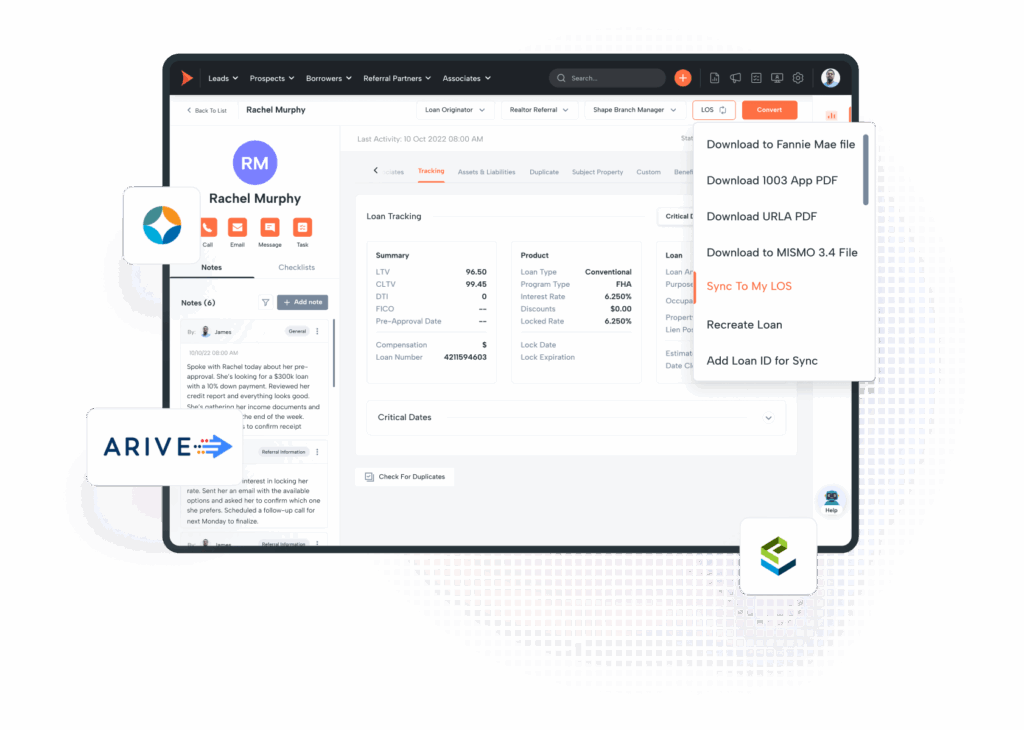

Shape’s native LOS integrations with Encompass, LendingPad, LendingDox, and more keep your pipeline moving with real-time updates, milestone syncing, and automated follow-ups—no manual data entry required.

Auto-sync loan data, milestones, and assignments

Send real-time updates to borrowers and partners

Keep agents and transaction coordinators in the loop

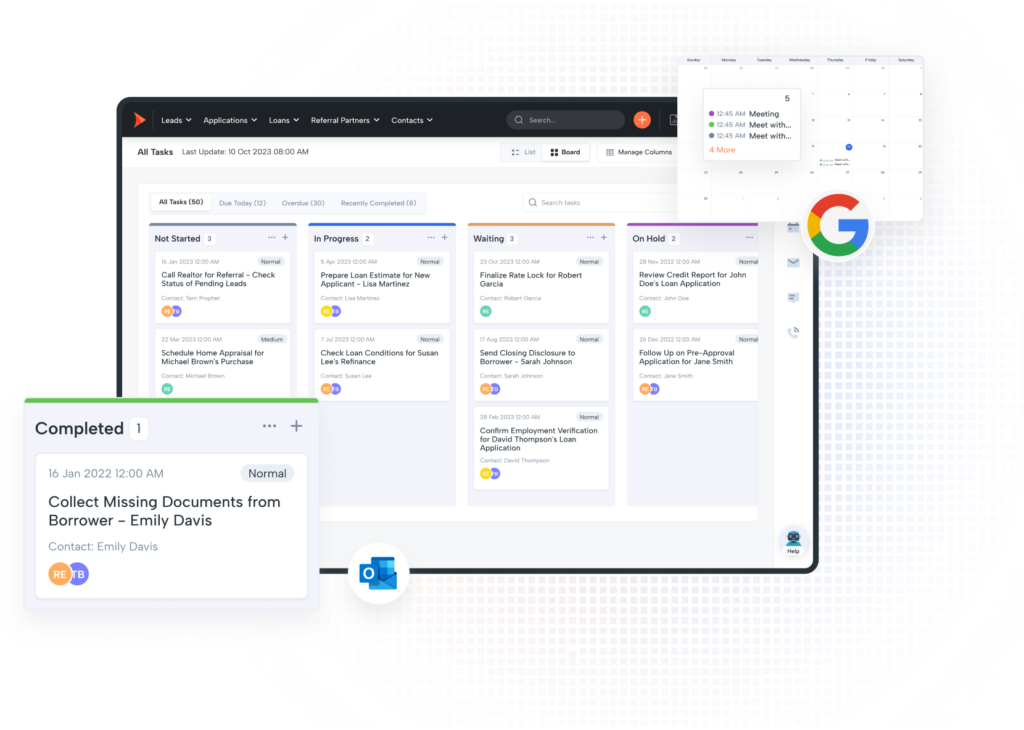

Manage daily to-dos and stay organized with built-in task tracking and seamless calendar sync to Google and Outlook—designed for busy loan officers who need everything in one place.

Set one-off or templated tasks with cadences

Build checklists tied to specific workflows & roles

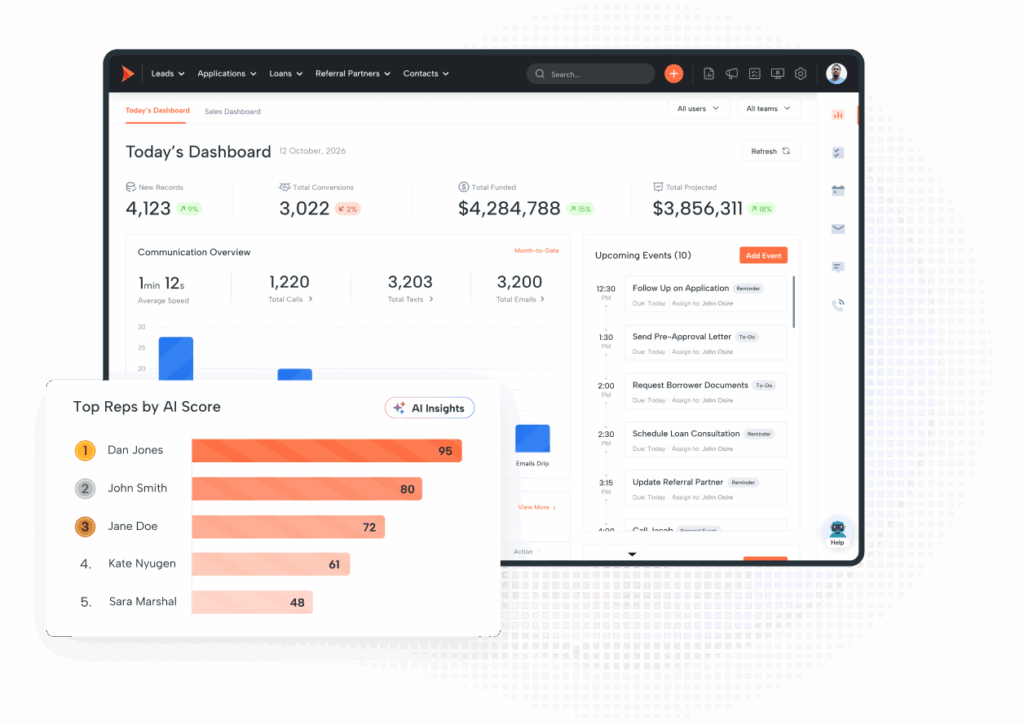

Track performance, lead conversion, and marketing ROI with Shape’s built-in reporting tools—giving you the data you need to improve campaigns, train your team, and grow faster.

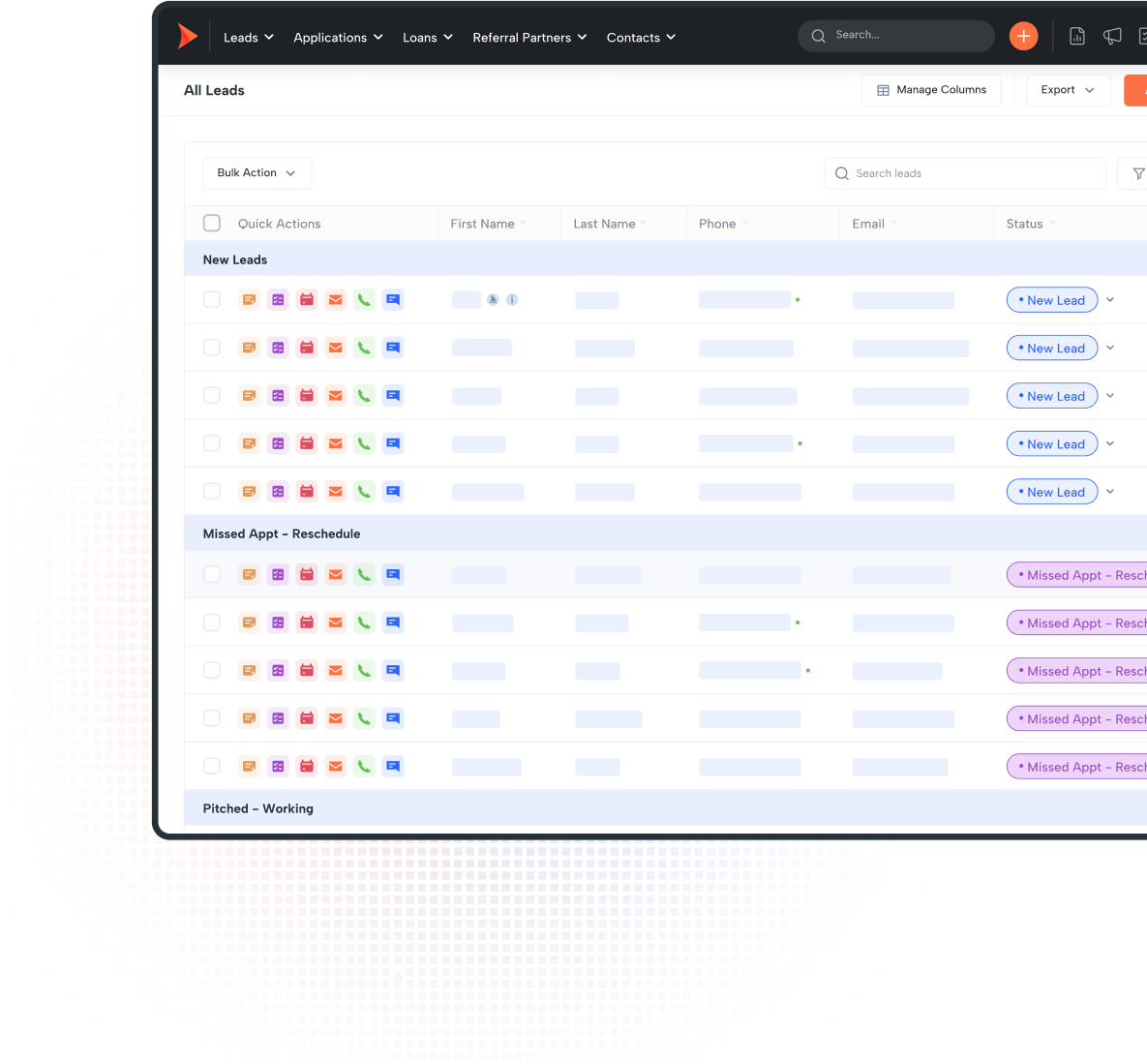

Shape’s lead management tools help you route, prioritize, and convert faster — with built-in compliance, duplicate prevention, and high-volume routing built for mortgage teams.

Advanced Lead Distribution Logic

Customize lead distribution based on licensing, source, channel, or campaign. Set rules for state eligibility, volume limits, delivery windows, and lead type to ensure every mortgage lead is routed to the right loan officer instantly and compliantly.

Built-In Duplicate Management

Shape prevents duplicate leads from clogging your system by identifying matches based on phone number, email, or custom logic. Get alerts or auto-merge options to ensure your team works one clean record, every time.

Prioritized Lead Views That Surface Hot Prospects

Not all leads are created equal. Shape automatically prioritizes leads based on time, status, activity, and custom scoring — so your team always knows which records to work next.

Shark Tank-Style Lead Pools for Unworked Leads

Give unworked or aged leads a second life. Shape’s shark tank queues let you reassign neglected leads into a competitive claim pool, keeping opportunities from slipping through the cracks.

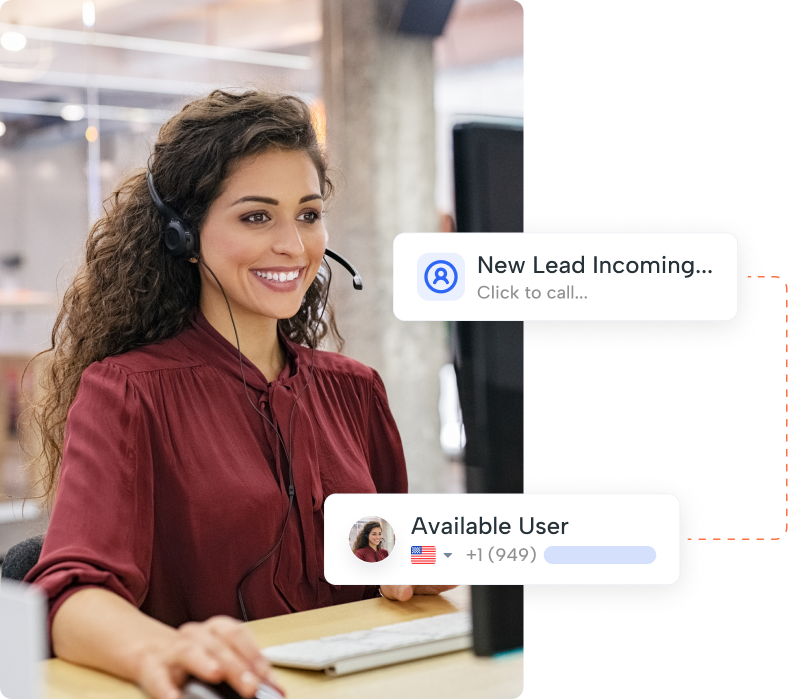

Everything you need to power smart, fast, and compliant phone communication — built right into Shape.

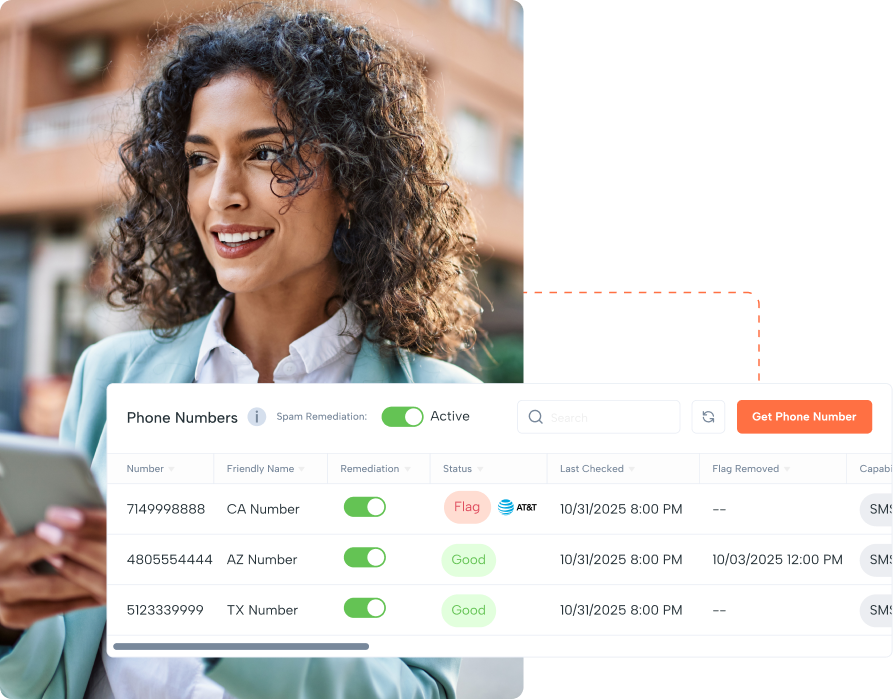

Local and Toll-Free Phone Numbers

Assign each loan officer a dedicated number for calling, texting, and MMS, or set up shared caller IDs for team-based outreach. Whether your setup is branch-driven or LO-specific, Shape gives you full control over how your numbers are used, tracked, and displayed — all while keeping communication seamless and professional.

Shape automatically selects the best outbound number based on your lead’s location — no manual work required. When prospects see a local area code on their phone, they’re more likely to answer, helping your team start more conversations and earn trust from the first ring.

In mortgage, seconds matter — especially with high-intent leads from competitive sources like LendingTree or Zillow. Shape instantly alerts your team when a new lead comes in and routes the call automatically through QuickFire Connect, so you're first on the phone — not the fifth. Faster response = higher conversions.

Whether you’re handing off a lead or escalating a pre-approval call, Shape gives you flexible transfer options — warm, cold, or no-hold transfer, which connects to the next available team member without missing a beat. No dropped calls, no missed opportunities — just a smoother experience that keeps the deal moving.

Shape can automatically record all inbound and outbound calls and attach them to the contact record for easy access. With ShapeAI Insights, every conversation is also transcribed, scored, and summarized — giving your team the visibility they need for coaching, compliance, and confidently moving deals forward.

Shape’s Heads Up Display lets managers listen in on live calls without interrupting the conversation or alerting the borrower. Ideal for mortgage teams focused on coaching, quality assurance, and real-time support, this tool gives you full visibility into how calls are handled — exactly when it matters most.

Assign each loan officer a dedicated number for calling, texting, and MMS, or set up shared caller IDs for team-based outreach. Whether your setup is branch-driven or LO-specific, Shape gives you full control over how your numbers are used, tracked, and displayed — all while keeping communication seamless and professional.

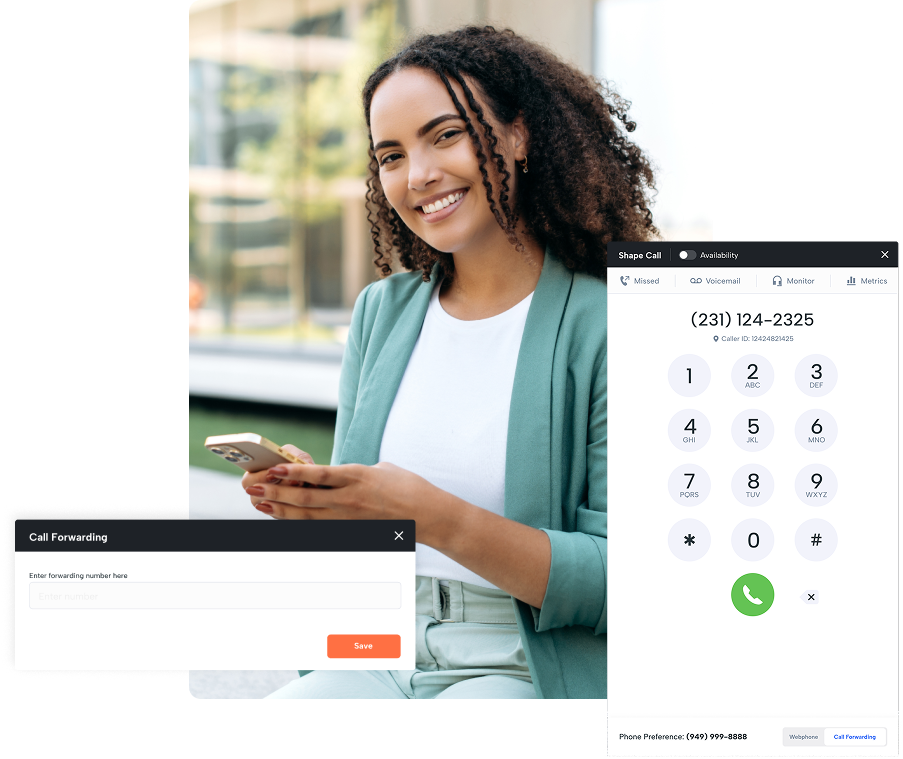

Never miss a borrower call — even when you're away. Shape lets you forward calls to your mobile device, office line, or another team member, making it easy for mortgage professionals to stay responsive after hours, while working remotely, or when stepping away from the desk.

Capture high-intent mortgage leads, convert faster with automation, and stay top of mind with powerful remarketing tools built into Shape.

Turn contact data into closings

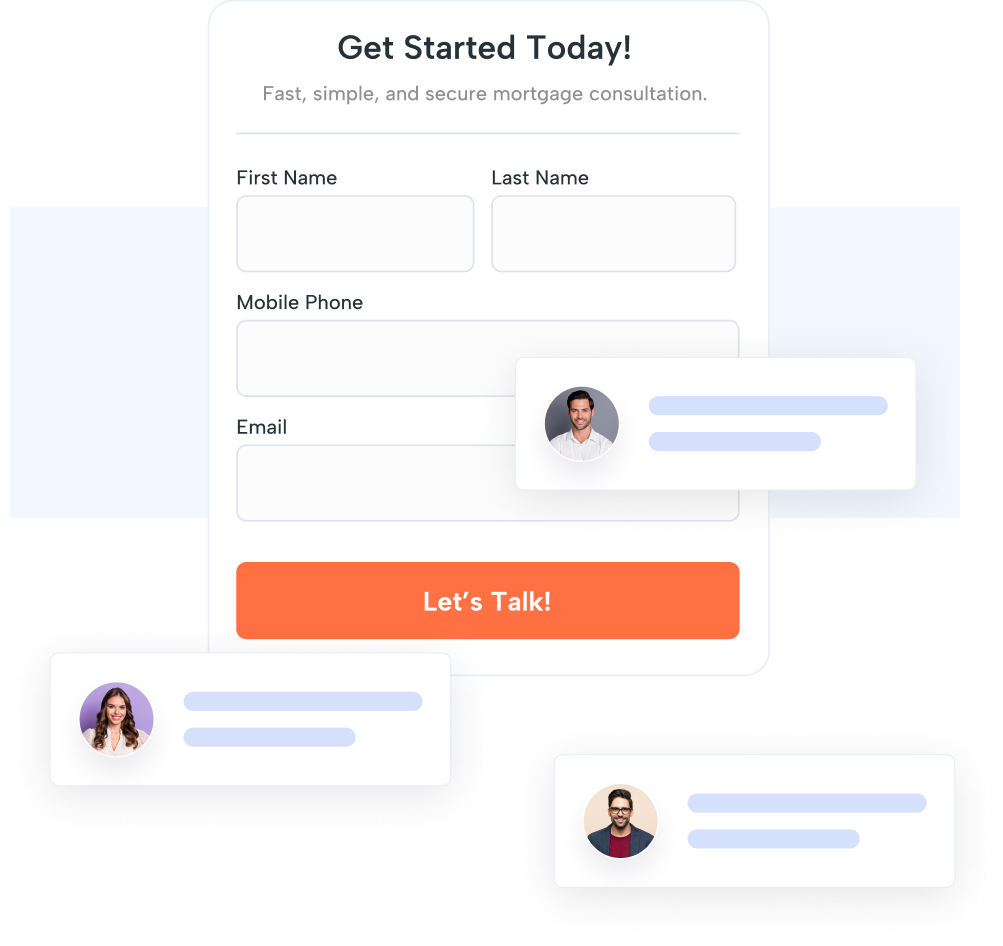

CRO-Optimized Landing Pages

Capture more mortgage leads with high-converting landing pages. Our team builds and customizes the pages for you — no coding or designers needed.

Borrower and Partner Contact Management

Manage all your borrower contacts and partners in one place — with source tracking, status updates, and a full history of every call, text, email, and task.

Data Hygiene for Smarter Follow-Up

Automatically verify contact records using trusted property and title data — so you can update addresses, confirm current residence, and focus your follow-up on the right borrowers.

Stay top of mind with pre-built mortgage campaigns that follow up automatically based on lead status, loan stage, or borrower activity — no manual work required. Keep your pipeline engaged from first inquiry to post-close.

AI Calling & Texting Assistants

From new mortgage leads to past clients, Shape’s AI assistants handle initial outreach, qualification, and appointment scheduling — giving your team more time to focus on meaningful conversations and moving loans forward. No voicemails, no phone tag, no wasted time.

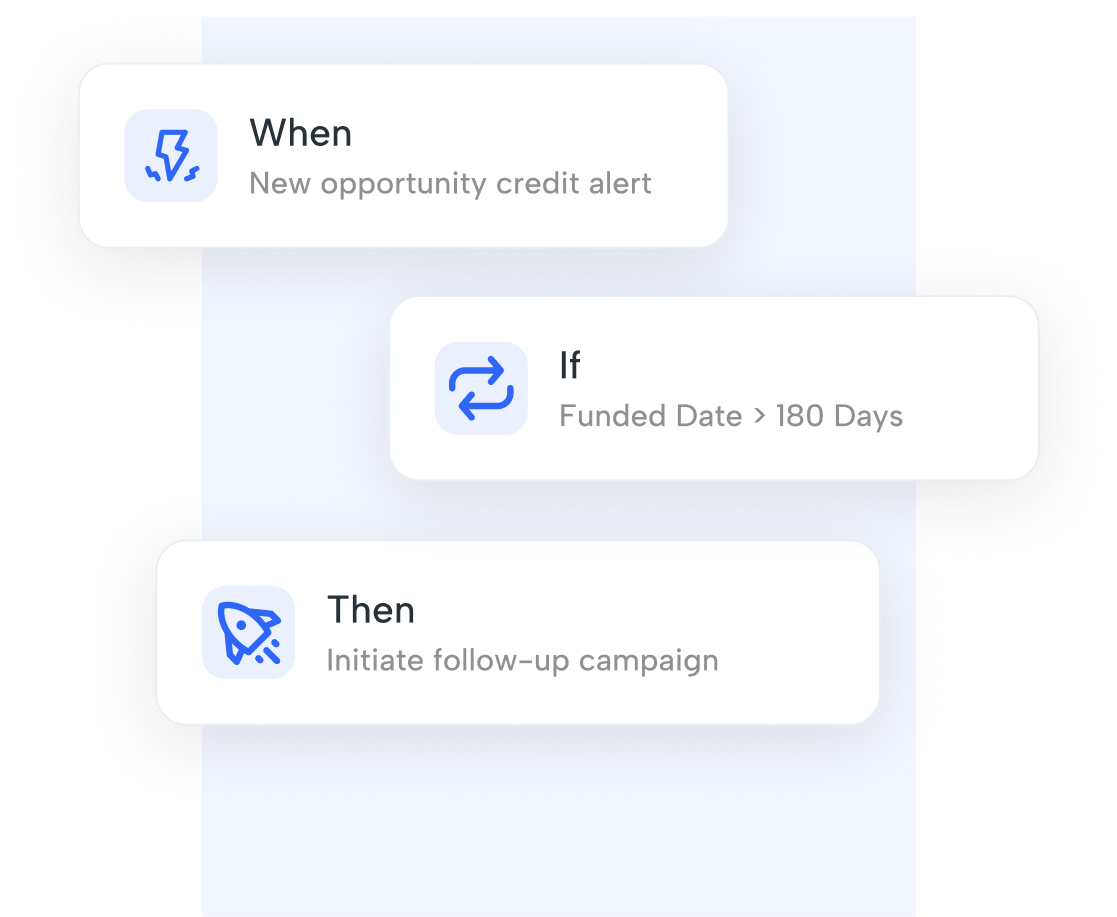

Credit and Intent-Based Trigger Alerts

Get real-time alerts when past leads take action — like a soft credit pull, mortgage inquiry, or rate check — so you can re-engage with perfect timing and win the deal before your competition does.

Shape’s built-in Design Studio lets mortgage professionals easily design marketing assets — from listing flyers to Instagram posts — without using external tools or designers. Print, publish, or send with just a few clicks.

Built-In Communication Tools

Every borrower conversation is tracked in one place. Use click-to-call, pre-built templates, and two-way texting to connect instantly and close faster.

Mobile App, Always On

Call, text, email, and manage leads on the go — whether you’re at an open house, traveling, or away from your desk. Everything stays synced, so you never miss a follow-up or status update.

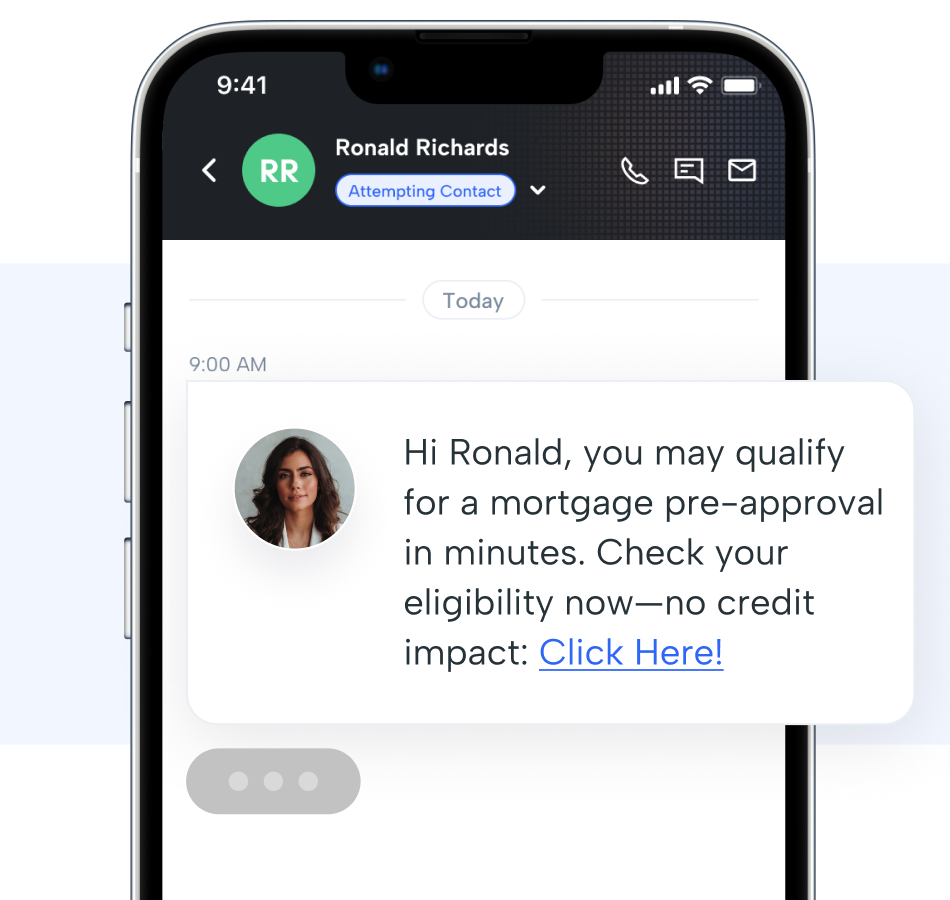

ShapeAI picks up when you can’t. Our inbound AI assistant answers calls, greets leads by name, collects intent, and offers to transfer or schedule a callback. Whether it’s 10 AM or 10 PM, inbound leads are acknowledged instantly, with outcomes logged directly into the CRM.

00:00

AI Outbound Dialing

ShapeAI can proactively call new leads, old prospects, or follow-ups on your team’s behalf. Use AI to qualify, engage, and warm up contacts, then hand off hot conversations to a loan officer. Great for cold leads, missed connections, or reactivating your database.

00:00

AI Text Messaging

ShapeAI Texting helps you stay in front of every lead without sounding robotic. Whether you're confirming appointments, collecting docs, or following up on a pre-approval, AI can handle the back-and-forth with friendly, on-brand messages — and route replies to a human when it matters.

AI Calling Insights

With ShapeAI Insights, every recorded call is automatically transcribed, scored, and summarized. See how your team is doing, what borrowers are asking, and where conversations are going off-track — all without spending hours reviewing call logs.

Not just a CRM - your competitive advantage

Shape isn’t just a mortgage CRM — it’s the growth engine behind high-performing mortgage teams. Get the tools, support, and automation you need to move faster, stay compliant, and close more loans with less effort.

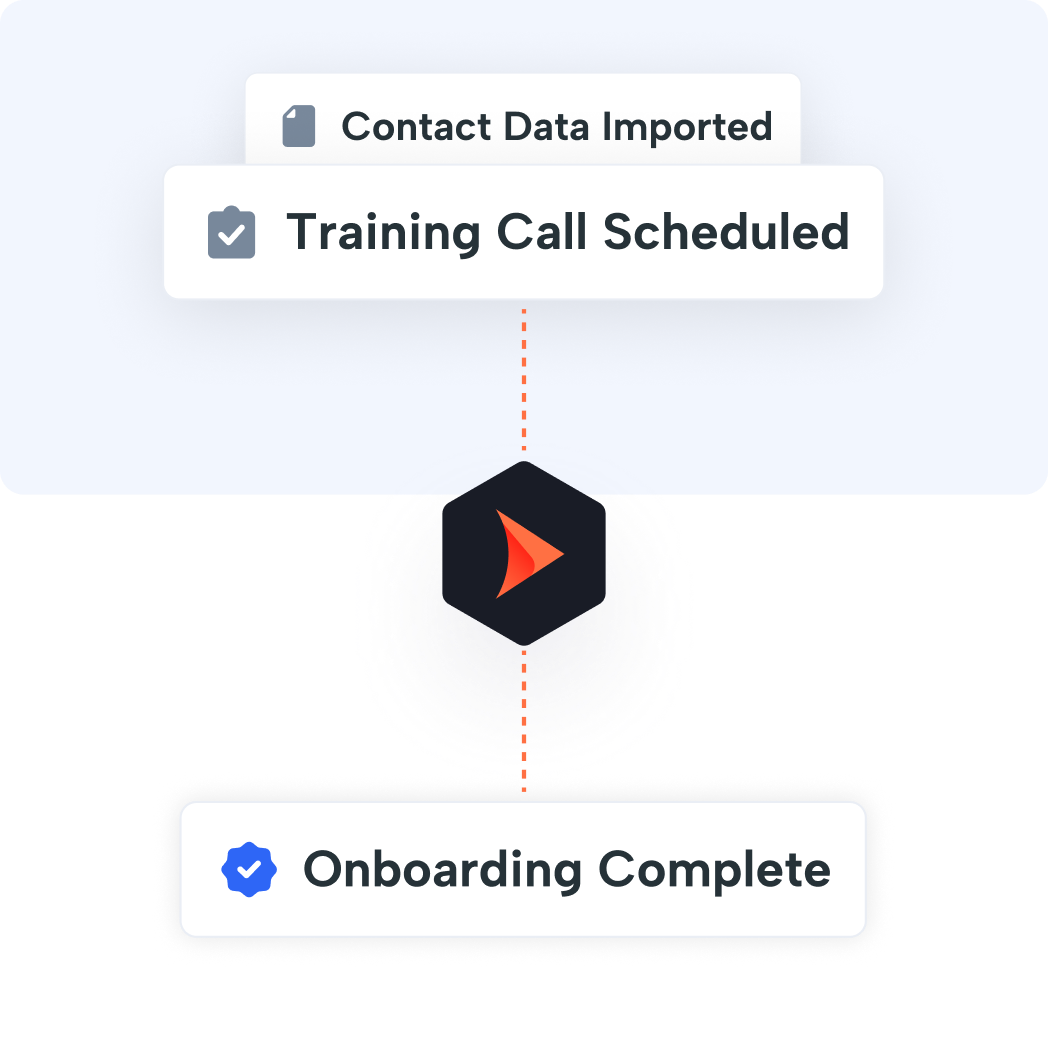

Launch Fast, Win Early

Get your team up and running in days, not weeks. Shape’s streamlined onboarding process helps you start managing leads and closing loans almost immediately. No complicated setup, no steep learning curve — just fast results from the start.

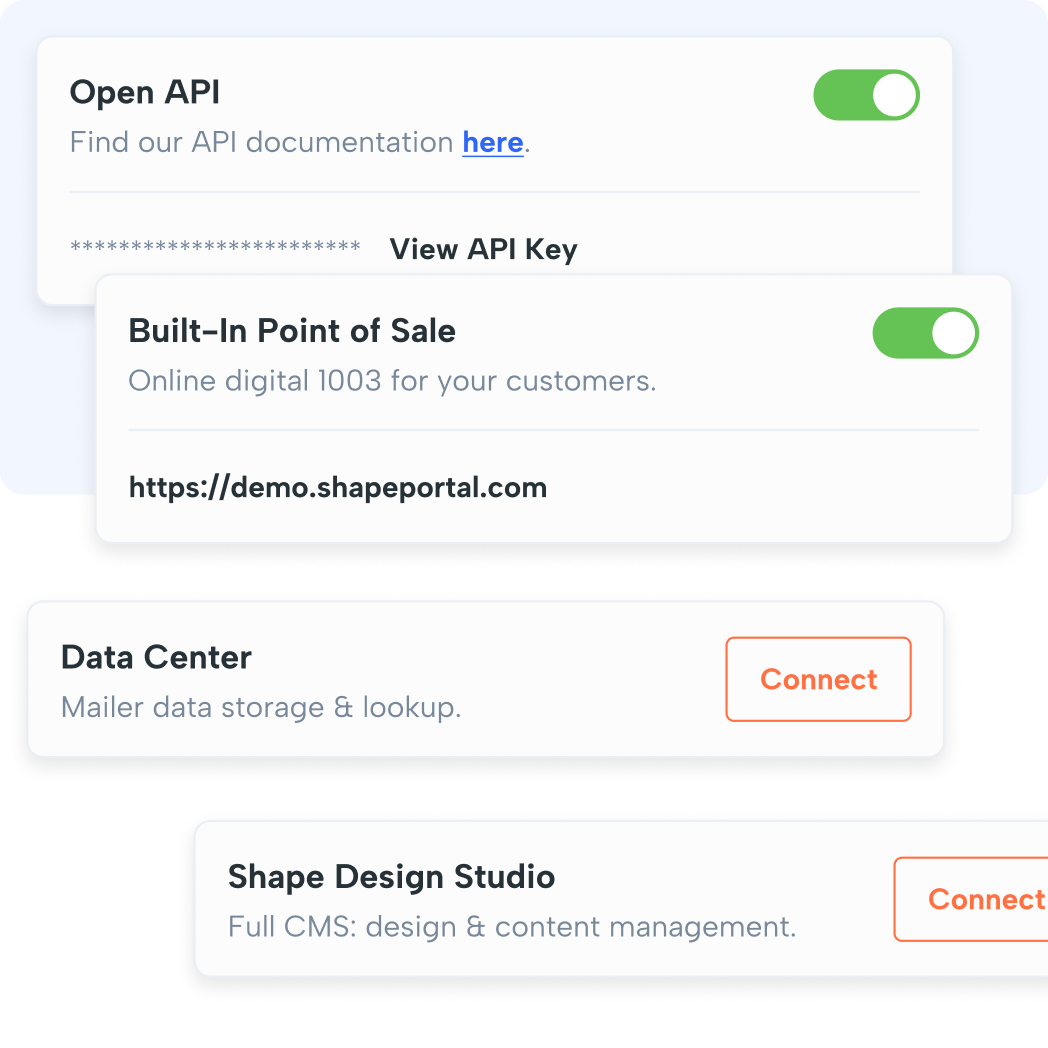

Built to Flex with You

As your business grows, Shape grows with you. With powerful API access, integrations, and expert-led solution design, you can customize workflows, expand capabilities, and adapt to changing needs — without ever outgrowing your CRM.

Loved by Mortgage Teams

Trusted by top lenders and brokers nationwide, Shape earns 5-star ratings for its speed, support, and results. Mortgage professionals choose Shape for its ability to streamline processes, simplify daily work, and deliver measurable ROI.

Compliance, Handled

Stay protected and audit-ready with built-in compliance safeguards. From DNC rules to 10DLC text regulations, Shape ensures every communication follows industry standards so your team can focus on serving clients with peace of mind.

Built for lenders, branches, brokers, and everyone in between

Whether you’re a solo broker or managing hundreds of loan officers across branches, Shape adapts to your workflow. Our tools are flexible enough for fast-moving teams and powerful enough for enterprise lenders.

Why lenders choose Shape

Built to support large teams, multi-branch operations, and complex workflows.

Two-way SMS/MMS with images, videos and emojis

Round robin, state licensing filters, caps, and more

Instant lead capture from all sources

Web, lead providers, and other third-party integrations

Bidirectional LOS integrations

Encompass, LendingPad, Arive, and others

Full pipeline visibility

Filter by user, branch, region, or channel

Role-based dashboards

Custom views for LOs, LOAs, processors, and managers

Milestone-triggered automation

Automatically follow-up at key stages like pre-approval, ctc, and funding

Centralized campaign management

Easily manage outreach across branches and departments

Built-in compliance tools

Includes support for 10DLC, TCPA, and DNC

Full admin control

Manage workflows, user roles, and team-level permissions

Scalable for any model

Works for retail, wholesale, consumer direct, or hybrid setups

See why lenders and brokers across the country rely on Shape to manage their leads, close more loans, and grow their business.

The company I work for made the move to Shape a year ago after I vetted out several CRM options. The move has been great for us. Shape Software along with Dani and her team have been exceptional to work with. We have a very complicated build-out for the system with in-depth customization. Shape worked with us to meet all of our needs and has gone out of their way to help us customize the system to our business model. We now use Shape for our CRM across multiple business channels and have worked with them to build lead capture pages with their secure-engine capabilities. I highly recommend the system and the Shape team.

- Benjamin Schott NFM Lending

We couldn’t be happier with our experience using Shape CRM, and a large part of that satisfaction comes from working with our account executive, Stewart Hartman. Stewart has been our project manager, and his dedication and expertise have been incredible. We evaluated many CRMs before deciding on Shape, and we are so glad we did. Stewart made the transition seamless and has been an invaluable resource every step of the way. His knowledge, responsiveness, and commitment to our success are unmatched. I highly recommend Shape CRM to anyone looking for a reliable and efficient CRM system — especially with Stewart Hartman leading the way. Thank you, Stewart, for your outstanding support and guidance!

- Rob Ross Intercoastal Mortgage

As a lifetime CRM user and trainer, Shape has integrated all the must-haves into one platform — both for the user and for gathering metrics for reporting. But a system is only as good as the support and team that helps you apply it to your business model. Dani and the rest of the Shape team have been incredibly communicative with our entire team and users. If you want to get a CRM and get the job done, I highly recommend working with Shape and Dani Dunn!

- Vanessa Reynolds AnnieMac Home Mortgage

Shape has been an absolute game-changer for my mortgage company. From day one, the platform has provided everything we needed to streamline our operations, improve communication, and ultimately scale our business. It's intuitive, powerful, and tailored to the needs of companies like mine.

- Abraham Gudino Coastal Pacific Lending

We've been using Shape Software for our mortgage business for the past two years, and it's been a game-changer. The platform is intuitive, reliable, and tailored to the needs of our industry. A special shoutout to Tristan from the Support Team—his responsiveness and dedication have made a huge difference. Whenever we've needed assistance, Tristan has gone above and beyond to ensure we’re supported. Highly recommend Shape Software for any mortgage professionals looking for a robust CRM with outstanding customer service.

- Dion Sloan Amerifund

Get started in 3 simple steps

No delays, no confusion — just a faster path to more funded loans with Shape Mortgage CRM.

See Shape in Action

Explore Shape in real time with a Shape expert. We’ll walk you through the platform, answer your questions, and show how it fits your team’s workflow.

We’ll Handle the Setup

From lead routing to LOS setup, we handle user access, integrations, and configuration so you can hit the ground running.

Start Closing with Confidence

Turn on automation, activate proven follow-up campaigns, and start converting faster with over 500 tools built to help you close more loans.

Frequently Asked Questions

Your mortgage CRM questions, answered

A quick guide to how Shape supports the way mortgage professionals actually work — no fluff, just facts.

Most teams are up and running in just a few days. We handle the initial setup, integrations, and training so you can focus on working leads, not configuring software.

Can Shape integrate with my LOS or POS?

Yes — Shape integrates with top mortgage LOS and POS platforms including Encompass, LendingPad, Arive, and SimpleNexus (nCino). We also offer a built-in digital 1003 loan application, borrower portal, and document upload tools. Our team will walk you through every step of setup and testing.

Does Shape include built-in calling and texting?

Absolutely. Shape includes built-in texting, calling, local presence dialing, call recording, and compliance tools like 10DLC and DNC support — no third-party dialer needed.

What types of automation can I use in Shape?

You can automate everything from drip campaigns and milestone-based borrower updates to lead status changes, task assignments, AI-powered calling, and intelligent text follow-up. Every workflow is customizable to fit your mortgage process.

What if I have multiple branches or teams?

Yes — Shape is built to support growing mortgage companies with multiple branches, teams, or divisions. You can route leads by branch, assign user roles, set team permissions, and track performance by group, region, or user.

Can my team use Shape from anywhere?

Yes — Shape is cloud-based and comes with a fully functional mobile app. Your team can call, text, email, and manage leads on the go, from any device.